Navigating India’s Debt Sustainability Amid Growth Headwinds

Aviral Akshat1, Chellsea Lauhka1, Poulami Sarkar1

aviralakshat.iitd@gmail.com, chellsea.lauhka31@gmail.com, poulamisarkar343@gmail.com1Indian Institute of Technology, Delhi

As India enters the mid-2020s, its fiscal outlook is drawing increased scrutiny. Public spending surged in the aftermath of the global pandemic, pushing up both central and general government debt-to-GDP ratios. These trends have sparked concern in policy circles and among international observers. The International Monetary Fund (IMF) has warned that under adverse conditions, general government debt could be near 100% of GDP by FY2027–28—particularly if climate-related investments rise without matching revenue efforts. Meanwhile, provisional GDP estimates for FY2024–25 show a slowdown to 6.5%, the weakest growth since the pandemic year of 2020–21. This mix of softening growth and elevated debt highlights the challenge of maintaining fiscal discipline while ensuring sustained public investment—both essential for India’s goal of becoming a $5 trillion economy and building climate resilience.

I. A Nuanced Debt Landscape

India’s central government debt-to-GDP ratio stood at 57.2% as of September 2024, barely changed from 57.1% in June. The government plans to raise ₹8 lakh crore in the first half of FY2025–26—about 54% of its full-year borrowing target. This borrowing plan has helped ease long-term bond yields.

While this central debt level remains below that of many advanced economies, the broader general government debt—which includes states—is much higher. According to the Reserve Bank of India, it was 86.5% of GDP in FY2022–23. This is a modest decline from the pandemic peak, but off-budget liabilities could push the real figure closer to 90%.

External debt has also grown significantly. It stood at $646.8 billion at the end of December 2023, up from $290 billion in 2010. Of this, 77% is long-term debt, and about one-third is owed to multilateral lenders like the World Bank and Japan—each accounting for 11% of the total. The share of external debt in total government liabilities has risen from 20% in 2010 to around 24% in 2023. This increase is partly driven by green bond issuances and financing needs linked to climate priorities.

II. Growth Moderation: Signals and Sectoral Patterns

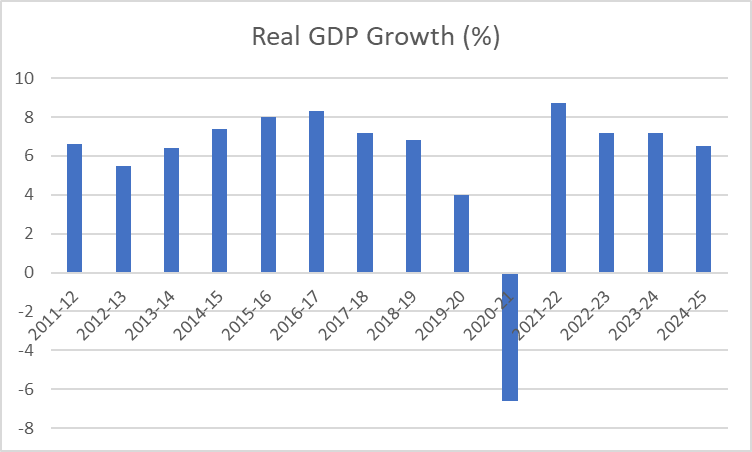

India’s real GDP grew at 6.5% in FY2024–25, the slowest pace since the COVID-induced contraction. According to provisional estimates from the Ministry of Statistics and Programme Implementation (MoSPI), Q4 FY2024–25 posted a stronger 7.4% growth. However, this still lagged behind the 8.4% expansion in the same quarter last year.

Figure 1: India’s Real GDP Growth (%) from FY2012 to FY2025.

The chart illustrates a steady growth trend with a sharp contraction in FY2020–21 due to the pandemic, followed by a strong rebound and recent moderation.

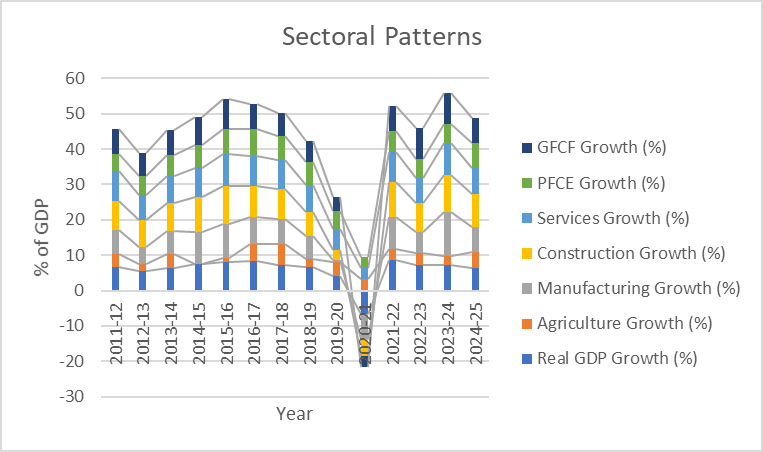

Sector-wise, agriculture rebounded sharply, growing 4.6% for the year. This was supported by a normal monsoon and stronger rural demand. Manufacturing, by contrast, slowed to 4.5%, down from 12.3% the previous year. The slowdown reflects global headwinds and muted private investment.

Construction remained a bright spot. It grew 9.4% for the year and 10.8% in Q4, buoyed by infrastructure and real estate activity—though still below last year’s pace. Services growth eased to 7.2%, compared to 9% last year. Within services, financial services and IT held up well, but travel and hospitality continued to underperform.

On the demand side, private final consumption expenditure (PFCE) rose 7.2%, signalling a post-pandemic consumption recovery. Gross fixed capital formation (GFCF) grew 7.1% for the year and accelerated to 9.4% in Q4, pointing to some recovery in investment sentiment.

Figure 2: Sectoral Growth Patterns as % of GDP (FY2011–12 to FY2024–25).

The graph captures the trajectories of GFCF, PFCE, and sectoral contributors like agriculture, manufacturing, services, and construction. Notably, all sectors witnessed a dip in FY2020–21, with uneven recoveries in the post-pandemic years.

Still, the overall moderation in growth is a concern. Slower nominal GDP makes it harder to bring down debt ratios. It also increases the burden of interest payments, especially if borrowing costs rise and growth doesn’t rebound.

III. Why Slower Growth Matters for Debt Sustainability

Fiscal sustainability depends heavily on economic growth. A slower pace of GDP expansion can worsen debt dynamics. India’s general government debt was 86.5% of GDP in FY2022–23 (RBI Annual Report), and a growth rate under 7% could drive this ratio higher, especially if climate spending grows without corresponding revenues.

Slower growth also erodes revenue buoyancy. While direct tax collections grew 18.7% in FY2023–24 (MoSPI), this pace could falter if the economy weakens. That would either force more borrowing or require fiscal austerity.

The interest burden is already substantial. Interest payments consumed 42.7% of the Centre’s revenue receipts in Budget 2022–23, leaving little room for welfare or infrastructure projects. With primary deficits projected at 1.5% of GDP in FY2025 (Statista), sustaining growth above 7% becomes vital to keeping debt from spiralling out of control.

IV. Charting a Sustainable Fiscal Path

To ensure debt sustainability, India must strike a balance between growth and fiscal prudence. The RBI estimates that general government debt can be stabilised at 85% of GDP by 2030 if real GDP grows at 6.5% annually and primary deficits are held near 2% of GDP.

Several reforms can support this path. Tax base expansion—especially through GST slab rationalisation, now under review—and further digitisation of direct tax systems have already borne fruit. Direct tax collections rose 18.7% in FY2023–24, pointing to gains from improved compliance.

Disinvestment and asset monetisation are also part of the fiscal toolkit. The government aims to raise ₹47,000 crore in FY2025–26 through these measures. Meanwhile, the National Manufacturing Mission targets a 25% share of manufacturing in GDP by 2047.

Improving the efficiency of public investment is another priority. Delays affect around 40% of central sector projects. Digitising project dashboards and amending land acquisition laws to fast-track infrastructure can help tackle these delays.

To stabilise debt, India needs to maintain real GDP growth of 7–7.5% and keep nominal primary deficits below 2% of GDP. Strengthening domestic capital markets is critical. Currently, corporate bonds account for just 18% of GDP, far behind China’s 80%.

India must also scale green finance. Sovereign green bonds already make up 24% of external debt. The RBI’s accommodative monetary stance, including a repo rate cut to 6% in April 2025, supports growth, but risks remain. Interest payments continue to consume 42.7% of central revenue, limiting fiscal space.

If managed well, fiscal stability will enable higher investments in climate resilience and social development, key pillars for inclusive growth as climate risks mount, a point the IMF has flagged repeatedly.

V. Conclusion: A Balancing Act in a Turbulent Environment

India’s fiscal landscape in 2025 presents cautious optimism. GDP growth has moderated to 6.5% in FY2024–25 (MoSPI), and general government debt remains high at 86.5% (RBI), while central government debt is at 57.2%. To avoid breaching IMF-cited danger thresholds, India must sustain growth above 7% and manage its debt with discipline.

CapEx continues to deliver strong growth multipliers, but execution challenges remain—about 40% of central sector projects face delays (Union Budget 2025–26). Reforms in land laws and digital tracking systems are essential.

Fiscal prudence—keeping primary deficits under 2% of GDP (IMF), broadening the tax base (18.7% direct tax growth in FY2023–24), and expanding green finance (now 24% of external debt)—is vital. These steps will attract ESG-focused investors and help fund India’s climate transition.

Policymakers must now institutionalise state-level debt ceilings, operationalise green finance frameworks (RBI), and avoid short-term fixes. If done right, India can convert its debt challenges into a platform for resilient and inclusive growth.

Comments

Post a Comment